{kind=link}

It’s hard to think of another U.S. government database that captures the entire history of American banking as completely as the FDIC BankFind Suite. From major Wall Street institutions to small rural branches that closed decades ago, this tool allows anyone to trace the full lineage of federally insured banks — all the way back to 1934.

For journalists, compliance analysts, or any citizen who wants to verify where their money is actually held, BankFind is more than a search form. It’s a transparency engine — a digital time capsule revealing who regulates a bank, when it was founded, what happened to it during mergers, and whether it’s still covered by federal deposit insurance.

Why the FDIC BankFind Suite Exists

The Federal Deposit Insurance Corporation (FDIC) was born out of crisis. Established in 1933 after thousands of banks failed during the Great Depression, its purpose was simple yet revolutionary: restore trust in the U.S. banking system by guaranteeing deposits.

Transparency was always part of that mission. If Americans were to trust their banks, they also needed a way to verify them. That’s where BankFind comes in. Originally a simple name-lookup tool, it has evolved into the FDIC BankFind Suite, a comprehensive public database of every FDIC-insured institution and branch — past and present.

Today, it remains one of the most important federal databases for financial accountability and consumer protection.

Inside the FDIC BankFind Suite

A Time Machine of American Banking

The BankFind Suite covers every FDIC-insured bank and branch from today back to 1934. This makes it a rare dataset that combines both historical and current information.

Researchers use it to reconstruct banking history — for instance, tracking how Wachovia Bank merged into Wells Fargo, or how local savings banks changed names and charters multiple times before consolidation.

Each record tells part of a larger story: when the bank was established, which regulator oversees it, and where its headquarters are located.

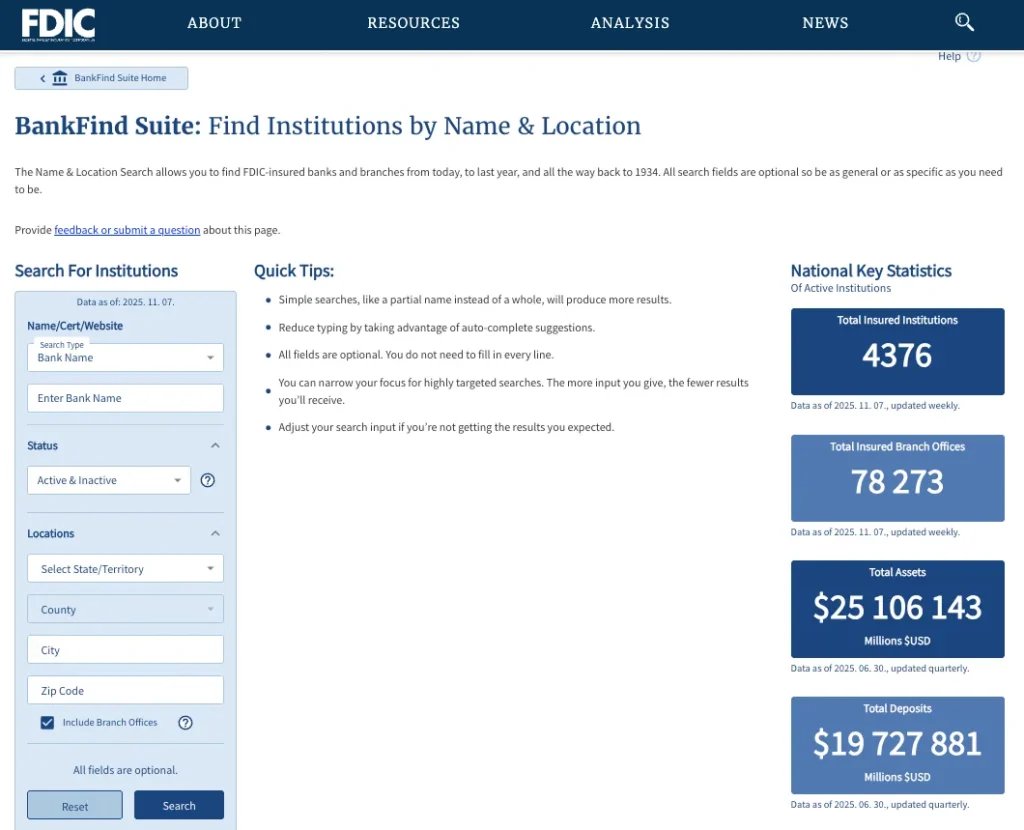

Search Options and How They Work

The database’s Name & Location Search tool is remarkably flexible. You can search by:

- Bank Name (partial or full)

- Type (commercial bank, savings association, etc.)

- FDIC Certificate Number

- Web Address / URL

- Status (Active, Inactive, Closed)

- Location (city, county, state, ZIP code)

All fields are optional — meaning you can be as broad or as specific as needed. The FDIC’s Quick Tips section even suggests that shorter, simpler search terms often yield better results, while more filters help narrow down large datasets.

It’s a design that works for both casual users and professional investigators.

What You’ll Find in the FDIC BankFind Suite Results

The Overview

A simple search — say, entering First National Bank of Omaha — produces an instant overview listing:

- Bank Name

- FDIC Insured (Yes/No)

- FDIC Certificate Number

- Primary Federal Regulator

- Headquarters Address

- Primary Website

At a glance, you can confirm if a bank is officially insured and who supervises it (often the OCC or Federal Reserve).

Going Deeper: “View Details”

Selecting View Details opens a full institutional profile with several sections:

- Institution Details: FDIC insurance status, charter class, regulator, headquarters, primary website, and contact options for consumer assistance.

- Locations: Every branch office, ZIP code, and service type, including dates established or acquired.

- History: A chronological log of significant events — mergers, name changes, relocations — each with an explanatory note.

- Financials: Core performance indicators drawn from regulatory filings.

- Other Names: Alternate institution names used over time.

For analysts, this depth of metadata transforms BankFind into a verified audit trail. It’s the backbone for understanding how banks evolve — or disappear — within the U.S. financial system.

How to Use FDIC BankFind Suite Effectively

Smart Search Techniques

To get the best results:

- Use partial names instead of full legal titles (“Community” instead of “Community National Bank”).

- Combine location filters (state or ZIP) when too many results appear.

- Use auto-complete suggestions to speed up typing and prevent spelling errors.

- If you don’t get expected results, simplify inputs — sometimes less is more.

These small adjustments often make the difference between frustration and discovery.

Verifying FDIC Insurance

The most common reason people use BankFind is to confirm FDIC insurance.

Every bank listed as “FDIC Insured: Yes” is backed by federal deposit insurance up to $250,000 per depositor, per insured bank — a cornerstone of consumer financial safety.

To check your bank:

- Type the institution’s name into the search bar.

- Select your branch or headquarters from the results.

- Look for the “FDIC Insured: Yes” label on the profile.

This quick verification ensures your deposits are covered by the U.S. government — not merely by private or state-level insurance.

For Journalists and Researchers

Investigative reporters, economists, and compliance officers frequently rely on the FDIC BankFind Suite to:

- Track bank mergers and acquisitions.

- Identify federal regulators for FOIA or oversight requests.

- Map community banking decline or regional concentration.

- Validate corporate structures against other public datasets.

For example, researchers often compare BankFind data with the NMLS Consumer Access Database — which lists licensed mortgage and nonbank lenders — to analyze overlaps between insured banks and non-bank financial institutions.

Similarly, for insurance sector analysis, the NAIC Database Insurance Check Guide provides a parallel transparency resource for verifying insurance company registrations.

Together, these systems build a broader open-data ecosystem of financial accountability.

Limitations and Transparency Gaps in the FDIC BankFind Suite

While BankFind is the official record, it isn’t perfect. Some older or smaller institutions have limited archival data, and the information relies partly on self-reported regulatory filings.

Also, non-FDIC entities — such as credit unions or fintech platforms — won’t appear here. To investigate those, you need other databases (like NCUA’s or state banking regulators’ systems).

Still, the FDIC deserves credit for maintaining one of the most consistent and accessible financial datasets in the federal government. Few public tools combine this level of historical continuity with near-real-time updates.

Why BankFind Still Matters in 2025

In an era of online banking, mergers, and digital-only financial institutions, a centralized government registry of FDIC-insured banks is not just helpful — it’s essential.

For consumers, it’s a safeguard. For regulators, a compliance checkpoint. And for journalists, a primary source for verifying claims about ownership, regulation, or insurance coverage.

As the financial industry evolves, tools like BankFind ensure that transparency evolves with it — preserving the public’s ability to follow the money, literally and legally.

Related Databases

- NMLS Consumer Access Database – For licensed mortgage lenders and non-bank financial service providers.

- NAIC Database Insurance Check Guide – For verifying insurance company registrations and regulatory oversight.

Sources

- FDIC BankFind Suite Official Database

- FDIC BankFind Suite Help Guide

- Federal Deposit Insurance Corporation – About FDIC

- FDIC Deposit Insurance Education Center

This article was created with AI assistance and reviewed by a human editor.