{kind=link}

If there is one habit that separates safe investors from victims, it is this: they check a broker’s background before handing over a single dollar. And in the United States, the most powerful tool for doing that is FINRA BrokerCheck. Yet most people still scroll past it—sometimes until it’s too late.

This guide breaks down how BrokerCheck actually works, what it reveals, what it hides, and how you can interpret a broker’s record the way an industry insider would. Whether you’re a retail investor, a journalist, or simply someone trying to avoid a costly mistake, this article will walk you through the system with real examples and practical steps.

Why FINRA BrokerCheck Matters More Than Ever

Financial advice is now accessible everywhere—Instagram, Reddit, TikTok, even inside online gaming platforms. The more informal the advice pipeline becomes, the easier it is for unlicensed or previously disciplined individuals to blend in.

In 2024, FINRA reported multiple cases in which barred brokers continued offering investment “tips” through social media accounts, camouflaging themselves as influencers. In one enforcement case, a previously suspended representative ran private investment groups through Telegram while marketing himself as a “retired Wall Street pro.”

The lesson is straightforward: appearance is not verification. BrokerCheck exists precisely because credentials, disciplinary history, and regulatory events cannot be reliably judged by a profile picture or confident tone.

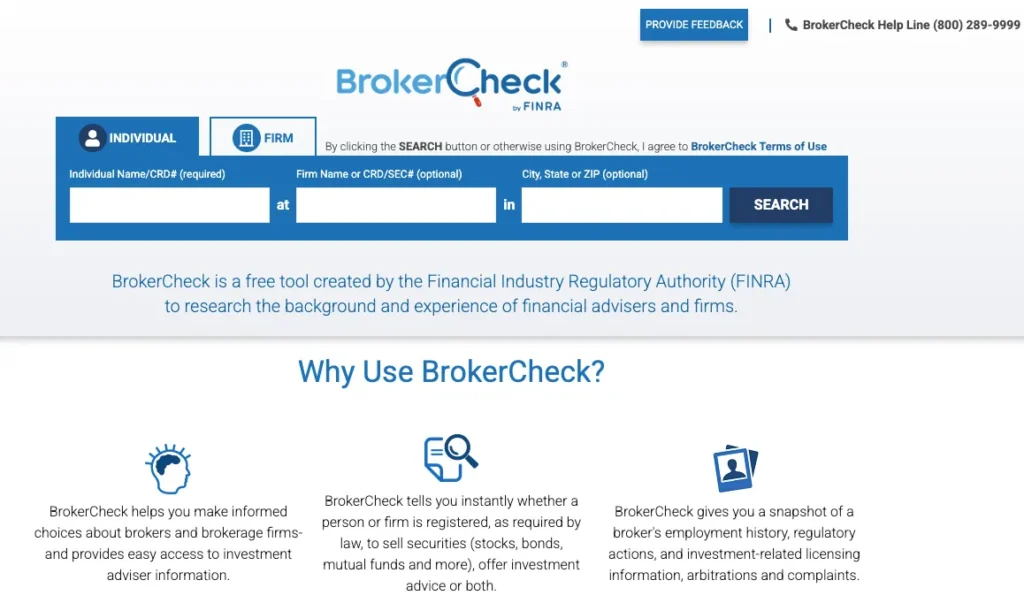

What Is FINRA BrokerCheck?

FINRA BrokerCheck is a publicly accessible database that allows anyone to look up licensed brokers, brokerage firms, and investment adviser representatives. It draws its information from the Central Registration Depository (CRD), the national licensing system used by regulators and firms across the United States.

BrokerCheck includes data from:

- FINRA

- SEC

- State securities regulators

- Brokerage firms (employment records, terminations, disclosures)

Its purpose is simple: to help the public make informed decisions about who they trust with their money.

On TheDatabaseSearch.com we frequently examine systems that enhance transparency in regulated industries. If you’re interested in broader tools for evaluating financial risk, our guides on the CFPB Consumer Complaints Database and the SEC’s EDGAR system provide additional context on how U.S. financial oversight databases operate.

What You Can Learn From a FINRA BrokerCheck Profile

Below are the most important sections of a BrokerCheck record—and how to read them like a professional compliance officer.

Licenses & Registrations

A legitimate U.S. broker typically passes exams such as:

- Series 7 (General Securities Representative)

- Series 63 (Uniform Securities Agent State Law)

- Series 65 or 66 for advisory activity

If a broker lacks these licenses, or recently terminated them, that is worth a closer look. A “registration withdrawn” entry may signal a voluntary career change—or it may follow a disciplinary event.

Employment History

BrokerCheck lists every firm a person has worked for, often reaching back decades.

⚠️ Red flag: a broker who has worked at 8–10 firms in a short period.

Frequent transitions can indicate internal performance issues, compliance problems, or conflicts with firm policies.

Customer Complaints & Disputes

This is the section most investors scroll to first—and for good reason.

You may see entries like:

- “Customer Dispute – Pending”

- “Customer Dispute – Settled”

- “Allegations: Misrepresentation, Unauthorized Trading”

A settlement does not mean the broker was innocent. It means the firm (often through insurance) resolved the claim financially. Patterns matter: three settled disputes often tell a clearer story than one large pending case.

Regulatory Actions

Regulatory actions can come from:

- FINRA

- SEC

- State regulators

- CFTC (if applicable)

A disciplinary action for misrepresentation, unsuitable recommendations, churning, or unauthorized activity should be taken seriously.

At TheDatabaseSearch.com, we also cover how to evaluate large financial datasets, such as the EDGAR Corporate Filings database, which is often used by analysts to investigate firms connected to advisors under review.

Bankruptcies & Financial Disclosures

A broker’s personal financial trouble does not automatically disqualify them. But it can be relevant.

Brokers facing repeated personal bankruptcies may have financial stressors that interfere with judgment.

What FINRA BrokerCheck Does NOT Show

This part often surprises readers. BrokerCheck is a powerful tool—but not a complete picture.

It does not include:

- Civil lawsuits unrelated to investments

- Misdemeanors (except those involving theft, fraud, or breach of trust)

- Criminal charges that are not felonies

- Civil protective orders

- Certain sealed or expunged matters

- Informal internal firm disciplinary notes

FINRA itself advises users to also check:

- The barred brokers list

- The SEC Action Lookup tool (for formal SEC actions against individuals, including non-brokers)

- State securities regulators (many maintain their own disciplinary databases)

In other words, BrokerCheck is a starting point, not a final verdict.

How to Use FINRA BrokerCheck (Step-by-Step Guide)

Step 1 — Visit the BrokerCheck Website

The official FINRA BrokerCheck website

Step 2 — Search by Name or CRD Number

Searching by CRD number is significantly more accurate, especially when the name is common.

Step 3 — Open the Summary Report

This page highlights key details: status, registrations, exams, disclosures, firm associations.

(Insert screenshot placeholder: BrokerCheck summary page)

Step 4 — Review Disclosures and Look for Patterns

A single disclosure may not be decisive.

Patterns—multiple disputes or sequential regulatory actions—are far more telling.

Step 5 — Compare With SEC IAPD When Relevant

Some advisors are dual-registered (broker + investment adviser).

Their SEC IAPD record may reveal advisory-specific issues not visible in BrokerCheck.

Example: How to Read a BrokerCheck Report (Fictionalized for Privacy)

Let’s imagine an advisor named John R. Malcolm (a fictional example).

His BrokerCheck report shows:

- Licenses: Series 7 and Series 66

- Employment: 4 firms in 6 years

- Disclosures:

- Customer Dispute – Settled (alleged unauthorized trading)

- Customer Dispute – Pending (unsuitable recommendations)

- Regulatory Action (2020): FINRA fine for failure to disclose outside business activities

How an expert interprets this:

- The combination of settled and pending complaints suggests behavioral consistency.

- The regulatory action aligns with the nature of the complaints—lack of transparency and oversight.

- Frequent job changes further reinforce the pattern.

Conclusion: This would not automatically indicate fraud, but it clearly warrants caution.

FINRA BrokerCheck vs. SEC IAPD — When to Use Each

Investors often confuse these two databases. They serve different regulatory worlds.

| Database | Best For | Overseer |

|---|---|---|

| FINRA BrokerCheck | Brokers, broker-dealers | FINRA + states |

| SEC IAPD | Investment advisers, RIA firms | SEC + states |

Many professionals appear in both systems. If you’re researching advisory services—portfolio management, financial planning, or fiduciary services—you should always check IAPD as well.

On TheDatabaseSearch.com, our guide to EDGAR Filings also explains how to use SEC datasets for deeper research into firms tied to a broker or adviser.

Additional Tools for Researching a Broker

BrokerCheck is essential, but not sufficient on its own.

Consider checking:

- FINRA Barred Brokers List

- SEC Action Lookup Tool

- State securities regulator disciplinary pages

- CFPB Consumer Complaint Database (contextual, not licensing-specific)

- Independent news searches for civil litigation

Often, regulatory databases capture only formal actions.

Civil cases and arbitration results may appear elsewhere.

Common Red Flags You Should Never Ignore

- Multiple customer disputes filed within a short timeframe

- Unexplained employment gaps

- Termination “for cause” (always read the details)

- Outside business activities involving real estate, crypto, or private lending

- Large settlements relative to assets under management

- Social media–based investment promotions that bypass firm compliance

These patterns rarely occur in isolation.

FAQs About FINRA BrokerCheck

Is FINRA BrokerCheck free?

Yes. FINRA operates it as a public investor-protection tool.

How accurate is the information?

It is updated regularly, but only reflects information FINRA is legally permitted to publish.

Can brokers remove disclosures?

They may request expungement, but the process is strict and overseen by FINRA arbitrators.

Does BrokerCheck show SEC or state issues?

Major regulatory actions typically appear, but always cross-check with SEC and state databases.

Does it show criminal records?

Only felonies and certain misdemeanors related to fraud, theft, or trust.

Conclusion: BrokerCheck Should Be Your First Stop—Not Your Last

FINRA BrokerCheck is one of the most powerful transparency tools available to U.S. investors. But like any database, it reflects only what regulators are permitted to publish. Used correctly—alongside SEC, state, and independent records—it can prevent devastating financial mistakes.

In an age where anyone can pose as a financial expert online, verification is not optional. BrokerCheck gives you the ability to look beyond marketing, confidence, or charisma—and examine the facts.

Sources and Authoritative References

Official Regulatory Databases

- The official FINRA BrokerCheck website

- FINRA Barred Brokers List – https://www.finra.org/rules-guidance/oversight-enforcement/finra-disciplinary-actions

- SEC Action Lookup Tool – https://www.sec.gov/enforce/public-alerts

- NASAA State Regulators – https://www.nasaa.org/contact-your-regulator/

- CFPB Consumer Complaint Database – https://www.consumerfinance.gov/data-research/consumer-complaints/

Relevant Financial Guides on TheDatabaseSearch.com

This article was created with AI assistance and reviewed by a human editor.